1 month ago

54

1 month ago

54

ARTICLE AD BOX

18 minutes ago

Kevin PeacheyCost of living correspondent

Getty Images

Getty Images

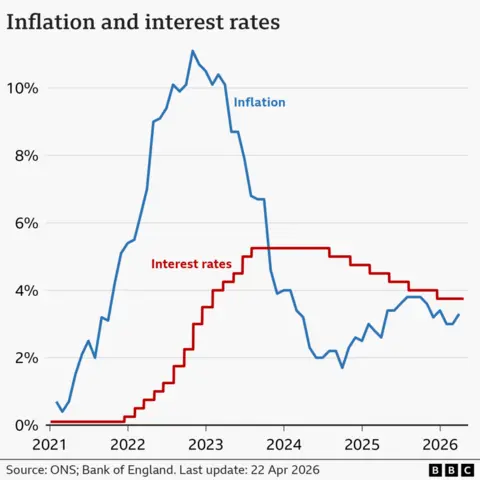

Interest rates are expected to be held at 3.75% by the Bank of England, with uncertainty dominating the UK and global economies.

Analysts are widely predicting the benchmark rate will be left unchanged owing to strong signals from the Bank that it will take time to assess the impact of conflict in the Middle East on the economy and the cost of living.

The base rate is the Bank's primary tool in controlling inflation, which charts the annual rise in prices of goods and services.

The rate of inflation remains above the 2% target, at 3.3%, but a cautious approach by the rate-setting committee at the Bank of England is expected.

"The repercussions of the [Iran] conflict are still keenly felt and uncertainty about how the situation could evolve also remains high, which will be key points the Monetary Policy Committee (MPC) will have to consider," said Sandra Horsfield, economist for wealth management group Investec.

After the decision is announced at 12:00 BST, the MPC will also publish its first full monetary policy report and set of economic forecasts since the US-Israeli strikes on Iran began in late February.

The Bank is unlikely to give any firm views on the future direction of interest rates.

Commentators also say there is plenty of uncertainty for the rest of the year, with some saying rate rises remain a possibility, while others think no change is more likely.

Before the US-Israel attack on Iran, economists had expected the inflation rate and interest rates to fall further this year.

The MPC's decision has an impact on borrowers and savers, as well as the investment and hiring decisions of businesses.

Upheaval created by the war in Iran has pushed up the cost of mortgages for homeowners getting a new fixed deal.

For borrowers, the interest rate on a fixed mortgage does not change until the deal expires, usually after two or five years, and a new one is chosen to replace it.

The average rate on a two-year fixed deal was 4.83% at the start of the conflict, but rose to a peak of 5.90%, according to financial information service Moneyfacts. That has now dropped slightly to 5.81%.

A host of lenders have announced cuts in the last 24 hours, but brokers say that fixed rate rises in the coming weeks cannot be ruled out.

"The standard advice in uncertain economic times stands: secure a mortgage rate you think suits your circumstances or looks reasonable value for money as soon as you can, then try to switch to a cheaper deal with the lender before your mortgage is due to complete," said Aaron Strutt, from mortgage broker Trinity Financial.

Savers will also be closely watching the outcome of the MPC meeting.

Interest offered on half of UK savings accounts can beat 3.75% - the current Bank of England benchmark rate - but it is usually those who have not switched provider for a long time who get the worst deal, according to financial information service Moneyfacts.

If prices rise sharply, then the buying power of those savings is diminished, especially if the interest received on those savings is poor.

English (US) ·

English (US) ·